")

Federal Reserve Chair Jerome Powell (Image Source: Reuters)

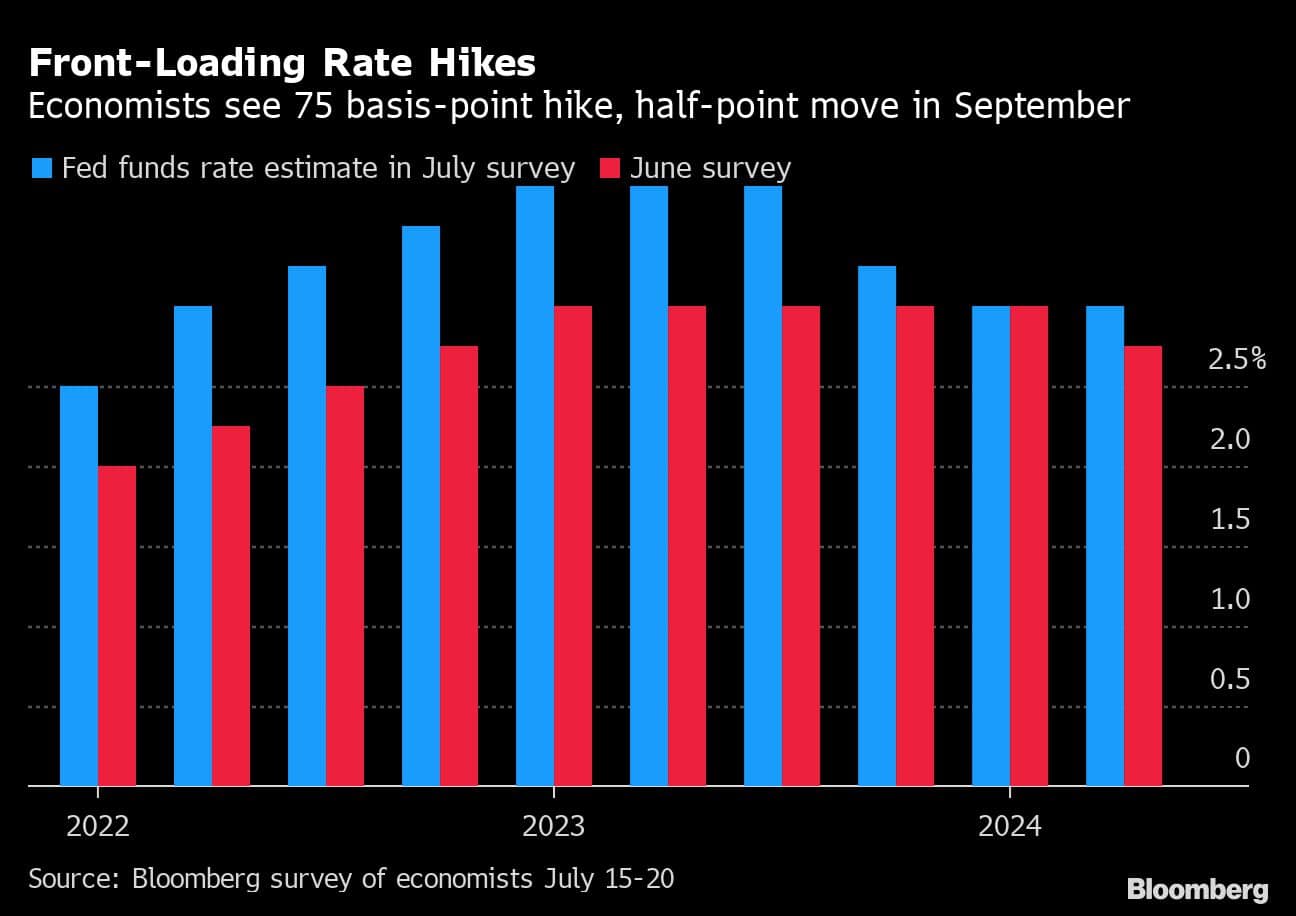

Federal Reserve Chair Jerome Powell is likely to slow the pace of interest-rate increases after front-loading policy with a second straight 75 basis-point hike this week, economists surveyed by Bloomberg said.

They expect the Federal Open Market Committee to lift rates by a half percentage point in September, then shift to quarter-point hikes at the remaining two meetings of the year. That would lift the upper range of the central bank’s policy target to 3.5% by the end of 2022, the highest level since early 2008.

Swap traders betting on Fed policy are now leaning toward a 50 basis-point hike in September as more likely than a 75 basis-point move, following weak US economic data earlier on Friday. The broader path envisioned by economists is slightly more hawkish than the one implied by market pricing.

It’s also steeper than what was expected prior to the June meeting, when the FOMC forecast rates rising to 3.4% at year’s end and 3.8% in 2023.

June’s 75 basis-point hike was the largest increase since 1994. Powell has said either 50 or 75 basis points would be on the table at the Fed’s July 26-27 meeting, though comments by many policy makers have centered on a 75 basis-point move.

The survey of 44 economists conducted from July 15 to 20 forecast the Fed will raise rates by another 25 basis points in early 2023, reaching a peak of 3.75% before pausing and starting to cut rates before the end of the year.

“The still strong labor market and solid consumer spending provide the leeway for the Fed to continue to quickly raise the policy rate,” Oxford Economics chief US economist Kathy Bostjancic said in a survey response.

There’s an overwhelming consensus that the FOMC will raise 75 basis points this month, with just one forecaster -- the US economics team at Nomura Securities -- looking for an increase of a full percentage point. Fed Governor Christopher Waller, one of the more hawkish policy makers, has endorsed a 75 basis-point move, and Atlanta Fed President Raphael Bostic warned that moving too dramatically would have negative spillover effects.

What Bloomberg Economics Says...

“Bloomberg Economics believes a 75-bp hike strikes the correct balance. The risk that inflation will trend upward is high. With Covid cases surging again and the war in Ukraine still raging, it’s likely we haven’t seen the last adverse supply shock. And with inflation expectations already on shaky grounds, the Fed needs to act preemptively before expectations become unmoored.”-- Anna Wong, Yelena Shulyatyeva, Andrew Husby and Eliza Winger

The Fed is seeking to cool off economic demand in response to surging prices that have persisted longer than expected and raised concern that inflation expectations could become unhinged. The consumer price index rose 9.1% in June from a year earlier in a broad-based advance, the largest gain since 1981.

If the Fed does deliver another 75 basis-point move next week, the combined increase of 150 basis points over June and July would represent the steepest rise in Fed rates since the early 1980s when Paul Volcker was chairman and battling sky-high inflation. There’s no appetite for a full-point increase at any time during this rate cycle, in the view of almost all the economists in the survey.

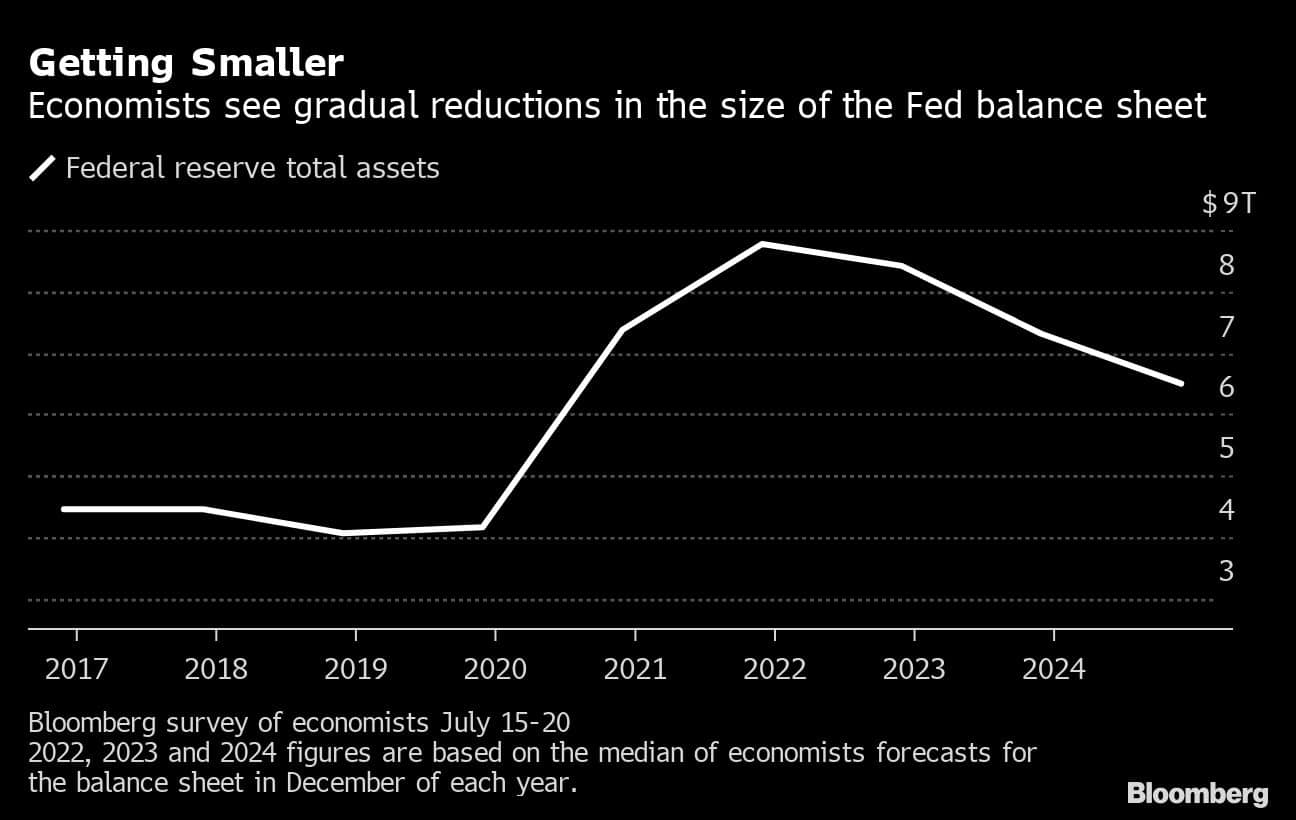

The economists expect the Fed to eventually step up its reductions in its balance sheet, which started this June with the runoff of maturing securities. The Fed is phasing in its reductions to an eventual pace of $1.1 trillion a year. Economists project that will bring the balance sheet to $8.4 trillion by year end, dropping to $6.5 trillion in December 2024.

Most of those surveyed say officials will resort to outright sales of mortgage-backed securities, in line with their stated preference to only hold Treasuries in the longer run. Among those expecting sales, there’s a wide range of views on when selling would begin, with most seeing it start in 2023 or later.

At the July meeting, the FOMC statement is expected to retain its language giving guidance on interest rates that pledges ongoing increases, without specificity on the size of the adjustments.

Most economists expect one dissent at the meeting. Kansas City Fed President Esther George, who dissented at the last meeting in favor of a smaller hike, has warned that too-abrupt changes in interest rates could undermine the ability of the Fed to achieve its planned rate path.

Wall Street economists have recently been raising more concerns about the potential for recession as the Fed tightens monetary policy amid headwinds including high energy prices and Russia’s invasion of Ukraine.

“The Fed is between a rock and a hard place; we can’t get out of the inflationary environment we are in with out suffering some pain and scars,” said Diane Swonk, KPMG LLP chief economist.

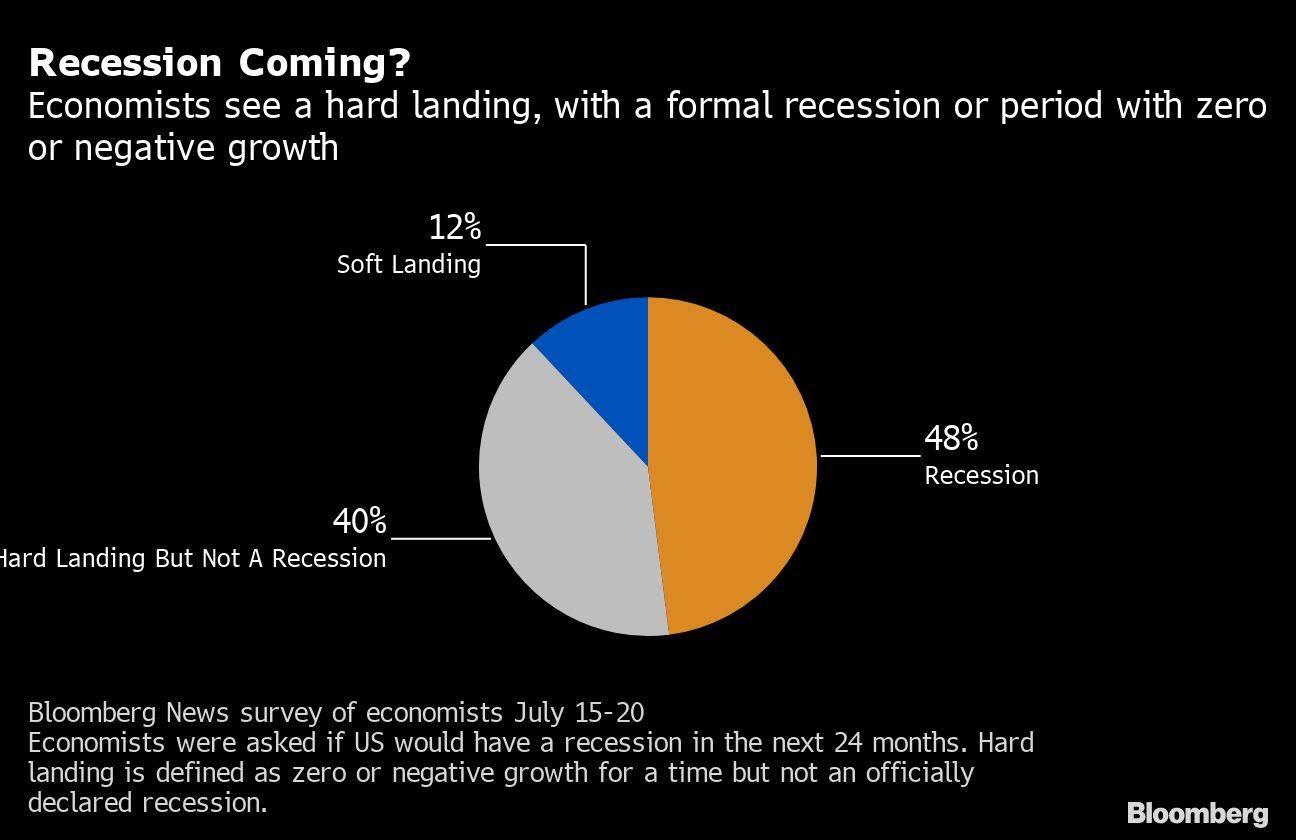

The economists are mixed about the outlook, with 48% seeing a recession as likely in the next two years, 40% seeing some time with zero or negative growth likely and the rest looking for the Fed to achieve a soft landing of continuing growth and low inflation.

While Fed officials have said they see persistently high inflation as the greatest risk they face, economists are divided, with 37% seeing inflation as the biggest risk and 19% seeing too much tightening leading to recession as the greater worry. The rest see the concerns as about equal.

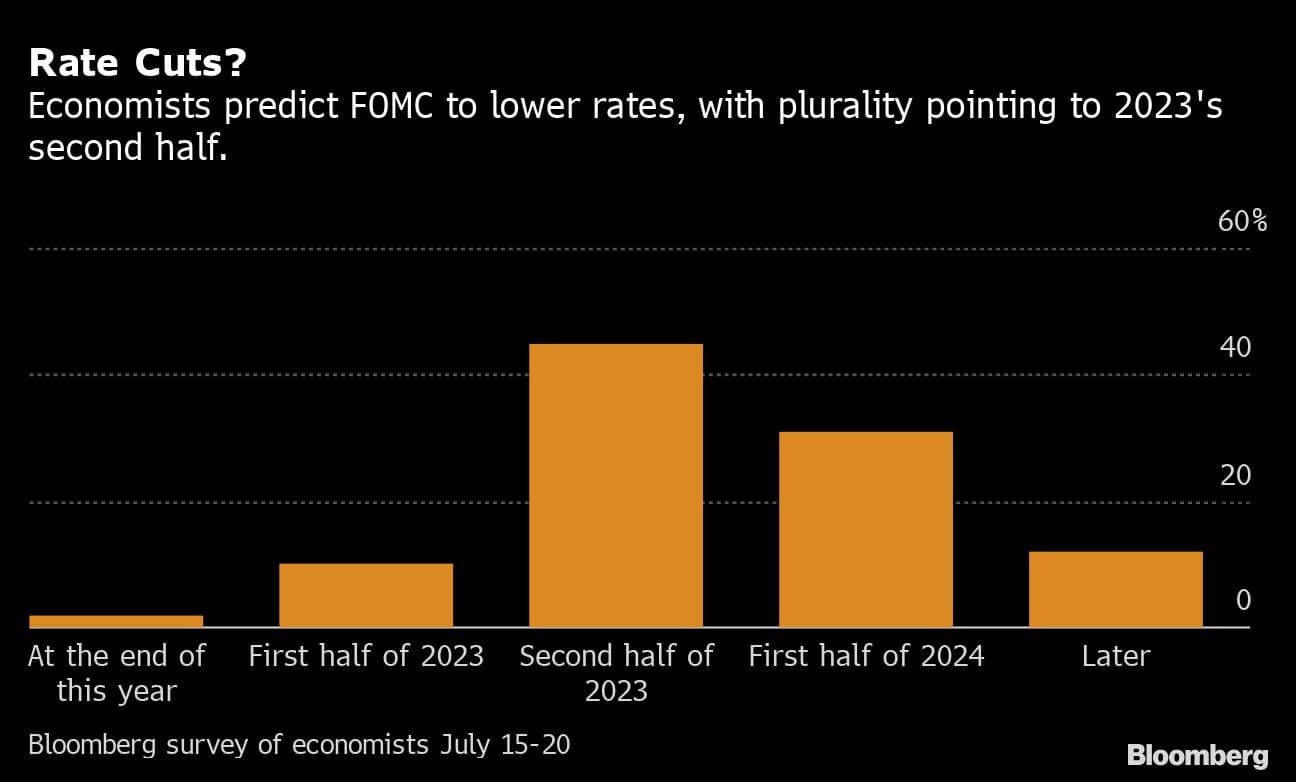

Beyond slowing rate hikes, the economists see the Fed eventually reversing course in response to lower growth and inflation. A plurality of 45% see the first rate reductions in 2023’s second half, while 31% expect cuts in the first half of 2024. By contrast, markets see peak rates reached by the first quarter of 2023, with a cut later in the year.

“Inflation should start to fall quickly from next March onwards as housing, used cars and gasoline prices look more favorable in year over year terms,” said James Knightley, chief international economist at ING Financial Markets. “This could open the door to a 2Q rate cut.”

Economists expect the central bank may stop its rate hikes well before inflation, measured by the Fed’s preferred metric, hits its 2% target. A plurality of 46% see the Fed halting its tightening with PCE core inflation, excluding food and energy, of 3.6% to 4%. Core inflation was 4.7% in May by that metric.Powell seen slowing Fed’s hikes after 75 basis points this week - Moneycontrol

Read More

No comments:

Post a Comment